Why updating your property valuation ensures success

- bryanlittle1

- Apr 12

- 9 min read

TL;DR:

Up-to-date property valuations are crucial due to recent market growth in Dublin and Kildare.

Using outdated figures can lead to longer sales times or missed financial opportunities.

Professional Comparative Market Analysis provides the most accurate and reliable property valuation.

Selling or letting your home in Dublin or Kildare without a current valuation is a gamble most homeowners cannot afford. Property values in both counties have shifted significantly in recent years, and even a modest pricing error can cost you thousands or stall your plans for months. Properties priced within 5-6% of accurate valuation sell noticeably faster, yet many sellers still rely on figures that are months or even years out of date. In this article, we explain why up-to-date valuations matter, how the local market has changed, which methods deliver the most reliable figures, and what pitfalls to avoid before you list.

Table of Contents

Key Takeaways

Point | Details |

Timely valuation increases sale success | Accurate, current valuations help you sell or let faster and avoid costly mispricing. |

Market changes require updates | Prices in Dublin and Kildare are rising and shifting—annual updates reflect true value. |

Use expert and online methods | Combine agent advice with up-to-date online data for the most reliable property valuation. |

Special cases need special approaches | Unique or rural homes require tailored comparisons and professional advice. |

Understanding why updating property valuations matters

Having set the stakes, let’s unpack the evidence for why a fresh valuation is vital in the current market.

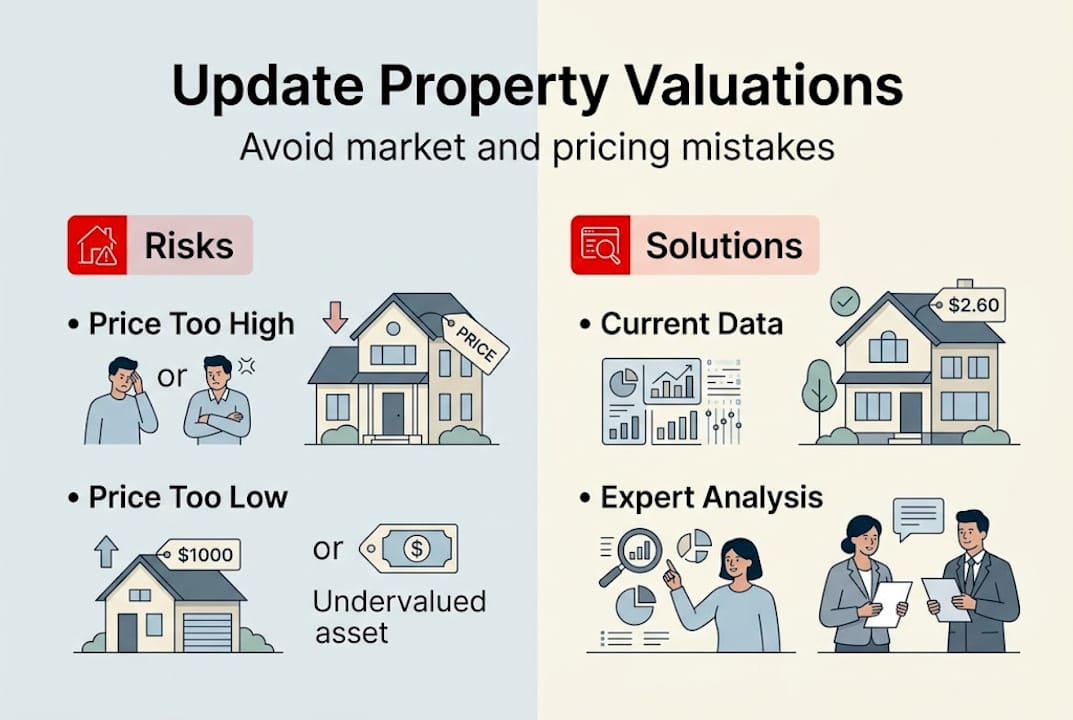

An outdated valuation creates two very different problems. Price too high and your property sits on the market, attracting fewer viewings and signalling to buyers that something is wrong. Price too low and you hand over equity you worked years to build. Neither outcome is acceptable, and both are avoidable with a current, accurate figure.

The numbers tell a clear story. National residential property prices rose 7% year-on-year by January 2026, with Dublin recording 6.1% growth and Kildare adding roughly €20,000 to its median value in a single year. If your valuation is even twelve months old, it is already lagging behind the market in a meaningful way.

The negotiation dynamic is equally important. There is a persistent 6% gap between asking and final sale prices in the local market. Buyers expect to negotiate, so your starting point must be grounded in real data. If you begin too high, you invite larger discounts. If you begin too low, you leave money behind before negotiations even start. Pricing your house right from day one is the single most effective strategy for a clean, fast sale.

Here is a quick comparison of what happens at different pricing positions:

Pricing position | Typical outcome |

5-6% above accurate value | Slower sale, more price reductions |

At accurate market value | Faster sale, stronger offers |

Below accurate market value | Quick sale but potential loss of equity |

For landlords, the same logic applies. Rental values in Dublin and Kildare have also risen sharply. Setting rent below the current market rate means leaving income on the table every single month. Understanding Irish property market trends helps you set a letting price that attracts reliable tenants at the right rate.

Overpriced properties typically take 30-60% longer to sell

Underpriced properties can attract multiple offers but close below true value

Stale listings lose credibility with buyers who track the market closely

Rental underpricing compounds over a twelve-month tenancy

Pro Tip: Before you agree on a listing price, ask your agent to show you the most recent three comparable sales in your area. If those sales are more than three months old, request updated data.

How updated valuations reflect real-time market changes

Once you know why accuracy matters, it is essential to see how prices and conditions evolve across both Dublin and Kildare.

The headline figures for early 2026 are striking. The Dublin median price reached €499,000 in Q4 2025, while Kildare’s median stood at €330,000, up €20,000 in twelve months. The national median sits at €390,000. These are not abstract statistics. They represent the real money you could gain or lose depending on whether your valuation reflects today’s market.

County | Median price (Q4 2025) | Annual change |

Dublin | €499,000 | +6.1% |

Kildare | €330,000 | +€20,000 |

National | €390,000 | +7% |

The RPPI rose 7% nationally in January 2026, confirming that the market is tightening rather than cooling. Supply remains constrained across both counties, while demand from commuter-belt buyers continues to push Kildare values upward at a pace that surprises even experienced agents.

“The Kildare commuter belt is one of the fastest-moving segments of the Irish residential market. Buyers priced out of Dublin are actively targeting towns like Naas, Newbridge, and Maynooth, creating genuine competition for well-presented stock.”

For sellers, this environment is favourable but unforgiving. A valuation from even six months ago may understate your property’s worth. For landlords, rental demand in both counties remains strong, and Kildare market trends show sustained upward pressure on achievable rents.

Here is how to keep your valuation current in a fast-moving market:

Check the Property Price Register every quarter for sales in your immediate area

Monitor Daft.ie and MyHome.ie for active listings near your property

Request a refreshed agent assessment every six to twelve months

Track recent Dublin market shifts through published market reports

Review the Dublin and Kildare market overview before committing to a listing price

Methods for obtaining an accurate property valuation

With prices in flux, here is how to get an accurate figure and ensure confidence in your listing decision.

The most reliable starting point is a Comparative Market Analysis, commonly called a CMA. This involves identifying three or more recently sold properties that are similar to yours in size, condition, location, and features. You then adjust the figures up or down based on differences. Agent CMAs are accurate within 3-5% of the achieved sale price, making them the gold standard for residential properties in Dublin and Kildare.

Online tools offer a useful reference point, but they have real limitations. Automated Valuation Models carry a margin of error of 10-20%, which on a €400,000 property means a range of €40,000 to €80,000. That is far too wide to base a listing decision on. A hybrid approach combining online data with an in-person agent assessment narrows this margin to 2-5%, which is genuinely useful.

Useful data sources for your own research include:

Property Price Register: The definitive record of all residential sales in Ireland, updated regularly

CSO Residential Property Price Index: Tracks national and regional trends month by month

Revenue’s valuation guidance: Provides a structured framework for property valuation in Ireland

Daft.ie and MyHome.ie: Show active asking prices and time-on-market data

Local estate agents: Offer the most granular, street-level insight available

Pro Tip: Use online tools to form an initial view, then book a free agent valuation to stress-test that figure. The combination gives you confidence without the cost of a formal independent appraisal in most cases.

Knowing when to go further than a CMA is important. If your property has unusual features, has been significantly extended, or sits in a micro-market with few recent sales, a formal valuation from a registered valuer adds an extra layer of certainty. For most standard residential properties, getting a professional valuation from a trusted local agent is sufficient and often free of charge.

Key nuances: special cases, LPT confusion, and energy ratings

After the standard process, you may encounter special scenarios. This section ensures you are ready.

One of the most common mistakes we see is homeowners confusing their Local Property Tax valuation with a current market valuation. These are entirely different figures. LPT valuations are fixed to November 2025 and will remain unchanged for the 2026 to 2030 period. They were designed for tax purposes, not for guiding sale or letting decisions. Using your LPT band as a proxy for your property’s current value could leave you significantly mispriced.

For rural or one-off homes, the challenge is finding meaningful comparables. If your property is unique in design, location, or size, the standard CMA process becomes harder. In these cases, unique properties should combine CSO and Revenue data with local agent knowledge and, where necessary, a formal independent appraisal. Do not rely on a single data point when your home falls outside the norm.

Building Energy Ratings (BER) have become a material factor in property values. A-rated homes can achieve up to 20% more than equivalent C-rated properties. Buyers and tenants are increasingly energy-conscious, and lenders are beginning to favour higher-rated properties with preferential mortgage terms. If your BER is low, it is worth understanding how this affects your achievable price before you list.

Key points to keep in mind for special cases:

Never use your LPT band as a guide to current market value

Rural properties need a broader data set and often a formal valuer

A poor BER rating can suppress your valuation price gap further

Extensions and renovations must be factored into any updated valuation

Probate, divorce, or shared ownership situations may require a formal RICS or SCSI valuation

“Your BER certificate is not just a compliance document. In today’s market, it is a pricing tool. Upgrading insulation or heating before listing can add real, measurable value to your sale.”

Our perspective: why some homeowners lose out and how to avoid their mistakes

Having seen the facts and the methods, here is what most people get wrong from our direct experience.

We see the same pattern repeatedly. A homeowner uses their LPT valuation as a mental anchor, or recalls what a neighbour’s house sold for two years ago, and builds their expectations around that figure. By the time they list, the market has moved and their price is either stale or simply wrong. The cost is not just financial. It is the stress of a property sitting unsold, the awkward price reductions, and the missed opportunity to move on with their plans.

Proactive homeowners do something different. They request agent assessments regularly, even when they are not immediately planning to sell. They treat their property’s value as a live figure, not a fixed one. Getting multiple agent inputs alongside online data consistently produces more accurate valuations and reduces regret after the sale completes.

The hidden cost of playing it safe is real. Waiting for certainty in a rising market means you are always one step behind. The 6% price gap risk is not theoretical. It shows up in final sale prices every week across Dublin and Kildare. Our honest advice is simple: get a free agent assessment now, even if you are only thinking about selling or letting. The information costs you nothing and could be worth a great deal.

Get a professional, up-to-date valuation for your property

If you are ready to act, getting a current, professional valuation is straightforward.

At RE/MAX Partners, we provide free, no-obligation property valuations for homeowners across Dublin and Kildare. Our team combines deep local knowledge with up-to-date market data to give you a figure you can actually rely on. No online calculator can replicate the insight that comes from knowing your street, your neighbourhood, and the buyers who are actively searching right now. Whether you are planning to sell or let, our property services for landlords and sellers are designed to get you the best possible outcome. Take the first step today and book a sales valuation with our team. We are here to help you move forward with confidence.

Frequently asked questions

How often should I update my property’s valuation in Dublin or Kildare?

You should update your valuation whenever you plan to sell or let, or at least annually. Market prices rose 7% year-on-year by January 2026, meaning a twelve-month-old figure is already out of step with current conditions.

Is my Local Property Tax (LPT) valuation suitable for selling or letting my home?

No. Your LPT valuation is fixed until 2030 and does not reflect real-time market movements, making it unsuitable as a guide for sale or letting prices.

How do estate agents value my house?

Agents use Comparative Market Analysis based on recent comparable sales, local demand, and your property’s specific features. Agent CMAs are accurate to within 3-5% of the achieved sale price in most cases.

What if my home is unique or rural?

You will need a broader approach. Unique properties benefit from combining national CSO and Revenue data with local agent insight and, where necessary, a formal independent appraisal from a registered valuer.

Recommended

Comments