Understanding rental yield in Ireland: guide for investors

- bryanlittle1

- Mar 22

- 8 min read

Property investment in Ireland demands more than intuition—it requires precise understanding of rental yield to assess genuine returns. Many investors treat rental yield as a fixed or straightforward percentage, overlooking critical variations between Dublin neighbourhoods, Kildare’s emerging market, and the substantial difference between gross and net calculations. This guide clarifies rental yield metrics with current data from Ireland’s property landscape, equipping investors in Dublin and Kildare with the knowledge to maximise returns through informed decision-making and realistic profitability assessments.

Table of Contents

Key Takeaways

Point | Details |

Gross and net yield | The gap between gross and net yield can be 2 to 3 percentage points, making net yield essential for mortgage approval. |

Dublin yield variance | Dublin city centre typically yields 4 to 6 per cent gross, while outer areas such as Dublin 10 and Dublin 22 can reach about 9.4 per cent for two bed homes. |

Kildare market growth | Kildare shows rental demand growth but lacks fixed yield benchmarks, so local market data is essential. |

Rent pressure zones | Rent pressure zones cap rent increases at two per cent per year or CPI, whichever is lower, potentially eroding future yields. |

Net yield costs | Mortgage interest, management fees 8 to 12 per cent, maintenance 1 to 2 per cent of property value, plus insurance, rates and vacancies all erode net returns. |

What is rental yield and why it matters

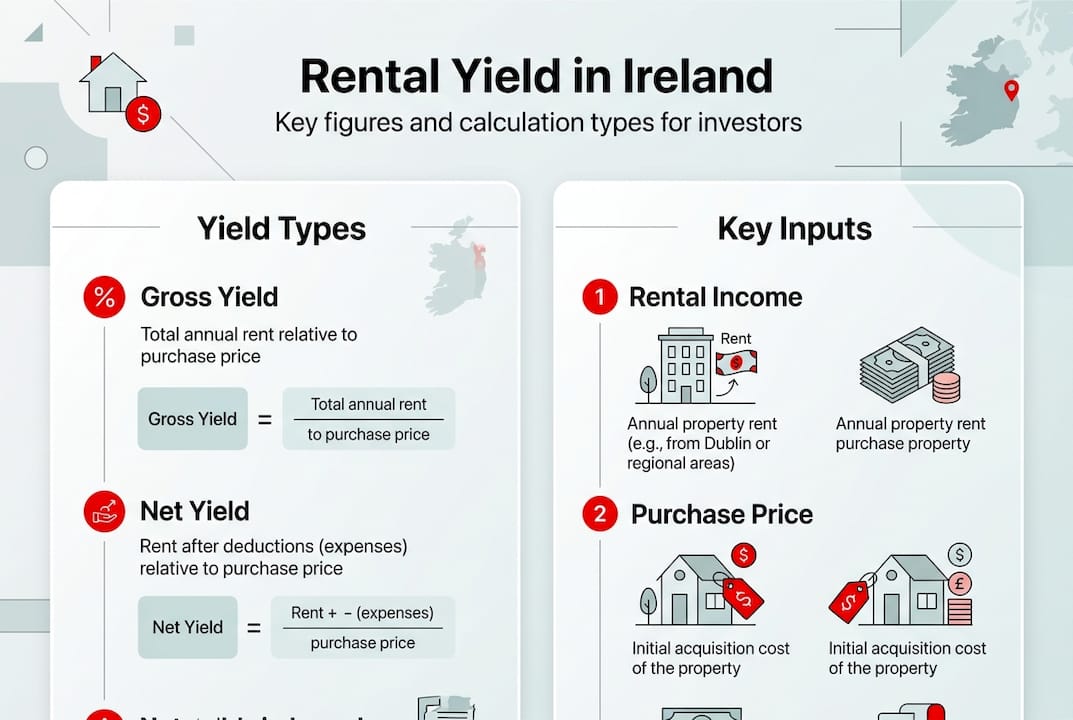

Rental yield represents the annual return on a property investment expressed as a percentage of the purchase price. Gross rental yield divides total annual rental income by property price and multiplies by 100. A property purchased for €300,000 generating €18,000 yearly rent produces a 6% gross yield. This figure provides a quick comparison tool but ignores the reality of ownership costs.

Net rental yield offers a more accurate profitability picture by subtracting expenses from rental income before calculating the percentage. Lenders require minimum rental yields for buy-to-let mortgages and assess income cover ratios between 125% and 145%, making net yield calculations essential for mortgage approval. The gap between gross and net yield can reach 2-3 percentage points, transforming an apparently healthy 7% gross yield into a modest 4.5% net return.

Rent pressure zones introduce another layer affecting yield calculations. RPZs limit rent increases to 2% annually or the Harmonised Index of Consumer Prices rate, whichever proves lower. This cap restricts landlords’ ability to adjust rents in line with market demand, potentially eroding yields over time as costs rise faster than permitted rent increases. Investors must factor this constraint into long-term profitability projections.

Costs impacting net rental yield include:

Mortgage interest payments reducing cash flow

Property management fees typically ranging 8-12% of rental income

Maintenance and repair expenses averaging 1-2% of property value annually

Insurance premiums for landlord-specific coverage

Local property rates and service charges

Vacancy periods between tenancies

Pro Tip: Monitor rental market indices quarterly to track yield fluctuations and adjust your investment strategy before profitability erodes. The house valuations and mortgage rates landscape shifts rapidly, and proactive investors who recalculate yields regularly maintain stronger returns than those relying on outdated assumptions.

Rental yield trends and benchmarks in Dublin

Dublin’s rental yield landscape reveals stark geographical variations that challenge city-wide generalisations. Dublin city centre apartments yield 4-6% gross, whilst outer districts like Dublin 10 and Dublin 22 achieve 9.4% for two-bedroom houses. This spread reflects property price differentials rather than rental income alone—central locations command premium purchase prices that compress yields despite higher absolute rents.

Dublin Area | Property Type | Gross Yield | Typical Property Price |

Dublin 1 (City Centre) | 1-bed apartment | 4.2% | €320,000 |

Dublin 8 (South Inner) | 2-bed terraced | 6.8% | €380,000 |

Dublin 10 (Ballyfermot) | 2-bed house | 9.4% | €240,000 |

Dublin 15 (Blanchardstown) | 3-bed semi-detached | 7.1% | €425,000 |

Dublin 22 (Clondalkin) | 2-bed house | 8.9% | €260,000 |

Property type and size significantly influence yield outcomes. Studios and one-bedroom apartments typically yield 6-8% gross in Dublin’s mid-range neighbourhoods, attracting single professionals and students willing to pay premium rents relative to property values. Larger three and four-bedroom family homes yield 5-7% in established suburbs, reflecting higher purchase prices and proportionally lower rental premiums.

The correlation between property prices, rental demand, and yield variation creates investment opportunities for those who analyse local data carefully. Areas with strong transport links to employment centres maintain consistent tenant demand, supporting stable yields even when purchase prices rise. Conversely, neighbourhoods experiencing rapid price appreciation may see yields compress as rental growth fails to match capital value increases.

Factors influencing Dublin rental yields:

Proximity to employment hubs and transport infrastructure

Supply and demand imbalances varying by neighbourhood

RPZ limitations constraining rent growth in designated areas

Property condition and age affecting maintenance costs

Local amenities and school quality driving tenant preferences

Pro Tip: Scrutinise precise local data for your target neighbourhood rather than relying on city-wide averages. A 2% yield difference between adjacent postal codes can represent thousands of euros annually. The Dublin housing market trends shift rapidly, and investors who track micro-market movements identify opportunities before they become obvious to the broader market.

Kildare’s rental market and yield considerations

Kildare presents a contrasting rental landscape to Dublin’s established yield benchmarks. Kildare rents increased 3% in Q3 2025, signalling growing tenant demand driven by Dublin’s overflow effect and improving transport connectivity. However, official rental yield data for Kildare remains limited compared to Dublin’s detailed neighbourhood breakdowns, requiring investors to conduct more thorough independent research.

The scarcity of fixed yield benchmarks reflects Kildare’s position as an emerging rental market rather than a mature investment destination. Properties in commuter towns like Naas, Newbridge, and Maynooth attract tenants seeking more affordable accommodation whilst maintaining reasonable access to Dublin employment. This dynamic creates yield potential but also introduces uncertainty around long-term rental growth sustainability.

Short-term rental opportunities present an alternative yield strategy in Kildare. Airbnb data indicates median annual revenues around $16,000 for properties in Newbridge, with high occupancy rates during summer months and racing season periods. This revenue stream can exceed traditional long-term rental yields by 20-30% but requires active management and carries regulatory risks as local authorities scrutinise short-term letting policies.

Factors affecting Kildare rental yields:

Local employment growth supporting independent tenant demand

Proximity to Dublin and commute times influencing rental premiums

Short-term rental policies and enforcement varying by local authority

New housing supply potentially increasing competition for tenants

Infrastructure improvements altering neighbourhood desirability

Evaluating Kildare properties requires a structured approach:

Research current rental rates for comparable properties using property portals and local letting agents

Assess short-term rental market potential through occupancy data and seasonal demand patterns

Calculate realistic expenses including higher vacancy rates than established Dublin markets

Evaluate long-term growth prospects based on planned infrastructure and employment developments

Monitor local authority rental policies and planning decisions affecting supply

Ongoing market monitoring proves essential in Kildare due to less stable benchmarks and rapid development patterns. The Kildare housing market trends demonstrate how quickly neighbourhood dynamics shift as new infrastructure projects complete and employment patterns evolve. Investors who treat Kildare as a static market risk miscalculating yields by 1-2 percentage points.

How to calculate and use rental yield effectively

Calculating rental yield accurately transforms abstract percentages into actionable investment decisions. Gross rental yield follows a straightforward formula but requires precise inputs to deliver meaningful results.

Calculating gross rental yield:

Determine total annual rental income by multiplying monthly rent by 12

Identify the property purchase price including acquisition costs

Divide annual rental income by purchase price

Multiply the result by 100 to express as a percentage

Compare the figure against benchmark yields for similar properties in the area

Net rental yield calculation demands more detailed expense tracking but provides the realistic profitability figure investors need. Subtract mortgage interest payments, property management fees typically 8-12% of rent, maintenance costs averaging 1-2% of property value, insurance premiums, and local rates from annual rental income. Divide this net income by the property purchase price and multiply by 100.

Property Example | Dublin 8 | Kildare (Naas) |

Purchase Price | €380,000 | €320,000 |

Annual Rent | €25,800 | €19,200 |

Gross Yield | 6.8% | 6.0% |

Mortgage Interest | €9,500 | €8,000 |

Management & Costs | €5,160 | €4,800 |

Net Rental Income | €11,140 | €6,400 |

Net Yield | 2.9% | 2.0% |

RPZ rules limiting rent increases to 2% or inflation directly impact future rental income projections. Accurate yield calculation must incorporate realistic rent values and expenses, considering RPZ caps and lenders’ income cover ratio requirements. An investor purchasing in an RPZ area cannot assume rental income will track market rates over time, potentially seeing yields decline relative to non-RPZ properties where rents adjust freely to demand.

Pro Tip: Regularly update yield calculations as rents and costs fluctuate to avoid profitability surprises. Recalculate quarterly using actual income and expense figures rather than initial projections. Investors who treat yield as a fixed metric at purchase time often discover their actual returns differ by 20-30% from expectations.

Using yield data alongside other metrics creates balanced investment decisions. Capital growth potential, neighbourhood development prospects, and tenant demand stability matter as much as current yield percentages. A 5% yield in an area experiencing 8% annual capital appreciation may outperform a 7% yield in a stagnant market over a five-year holding period. The Kildare and Dublin property valuations demonstrate how combining yield analysis with capital growth projections reveals the complete investment picture.

Explore property investment opportunities with RE/MAX Leixlip

Understanding rental yield mechanics provides the foundation for successful property investment, but local market expertise transforms knowledge into profitable decisions. RE/MAX Leixlip serves property investors throughout Dublin and Kildare with specialised services designed to maximise rental returns through informed property selection and professional management.

Our property listings at RE/MAX Leixlip feature buy-to-let opportunities carefully selected for strong rental yield potential across both established Dublin neighbourhoods and emerging Kildare markets. Each listing includes detailed rental market analysis and yield projections based on current local data, helping investors compare opportunities with confidence.

Beyond property sales, our comprehensive property services support investors throughout the ownership lifecycle. Professional rental property management handles tenant sourcing, lease administration, and maintenance coordination, ensuring your investment delivers projected returns without consuming your time. Our sales valuation services provide accurate property assessments essential for yield calculations and mortgage applications, backed by deep knowledge of local market conditions.

Contact RE/MAX Leixlip for expert advice tailored to your investment goals. Whether you’re evaluating your first buy-to-let property or expanding an existing portfolio, our team combines market data with practical experience to help you maximise rental returns in Dublin and Kildare’s dynamic property markets.

Frequently asked questions

How is rental yield calculated?

Rental yield divides annual rental income by property purchase price, then multiplies by 100 to express the result as a percentage. Gross yield uses total rent without deductions, whilst net yield subtracts expenses like mortgage interest, management fees, maintenance, and insurance before calculating the percentage. Net yield provides a more accurate profitability measure for investment decisions.

What rental yields can investors expect in Dublin and Kildare?

Dublin yields range from approximately 4% for city centre apartments to 9.4% in outer districts like Dublin 10 for two-bedroom houses. Kildare yields lack comprehensive benchmarks but show rental growth of 3% in Q3 2025 with strong short-term rental potential in towns like Newbridge. Investors should research specific neighbourhoods rather than relying on regional averages.

How do rent pressure zones affect rental yields?

RPZs cap rent increases at 2% or the Harmonised Index of Consumer Prices rate, whichever proves lower. This restriction limits landlords’ ability to raise rents in line with market demand, potentially reducing net rental yields over time as property costs and inflation outpace permitted rent increases. Investors must factor RPZ constraints into long-term profitability projections.

Should investors prioritise gross yield or net yield?

Net yield provides the essential profitability metric because it accounts for actual ownership costs reducing rental income. Gross yield serves as a quick comparison tool but can mislead investors by ignoring expenses that significantly impact returns. Lenders also assess net yield through income cover ratios when approving buy-to-let mortgages, making it the critical figure for both investment analysis and financing.

How often should rental yield calculations be updated?

Recalculate yields quarterly using actual income and expense figures rather than initial projections. Rental markets shift rapidly, and costs like maintenance and insurance fluctuate throughout ownership. Investors who update yield calculations regularly identify profitability issues early and adjust strategies before returns erode significantly, maintaining stronger long-term performance than those treating yield as a fixed purchase-time metric.

Recommended

Comments